Core view

In the second quarter, the three conditions of interest rate reduction may have marginal changes, which in turn will push interest rates down. (1) According to the market expectation, the Federal Reserve may start to cut interest rates in June, and the domestic wide monetary space may be gradually opened. (2) At present, domestic real estate investment and sales are still in a deep adjustment range. In the first quarter, the financial strength was less than expected, the issuance of special bonds was slow, the growth rate of infrastructure may be restricted, and the weak economic fundamentals may need further care from the broad currency. (3) From a medium-and long-term perspective, in the process of resolving local debt risks, for the needs of steady growth and reducing the cost of bond swap, or the cooperation of the central bank with a wide currency, and the real estate cycle has not yet reached an equilibrium level, the wide currency is still needed for support. Under the combination of "wide currency+weak fundamentals", interest rates may usher in new catalysis.

abstract

Since the first quarter, the interest rate of 10-year treasury bonds has continued to consolidate after falling to around 2.3%.It is difficult for the interest rate to exceed 2.3% in the short term, mainly because of the following two reasons: 1) The interest rate of 1)10Y national debt has implied the expectation of 20BP interest rate reduction, but at present, under the restriction of exchange rate, the probability of short-term interest rate reduction in China is low; 2) On the economic fundamentals, most macro data in January and February were better than expected, and the bond market was adjusted back due to the recovery of sentiment in the equity market and the seesaw effect of stock and debt. If the subsequent interest rate is to go down further, it may need the guidance of MLF to cut interest rates. What are the conditions for the next rate cut? We answer this question from overseas, domestic and medium-and long-term perspectives.

Condition 1: the exchange rate restricts interest rates and waits for the Fed to cut interest rates.

The exchange rate and interest rate have once again reached their respective low levels, and the supervision faces a dilemma, or it may need to wait for the Fed to cut interest rates.There are two main reasons for the recent depreciation of the RMB exchange rate: 1) In 2024, the resilience of the US economy is still strong, which is manifested in the stubbornness of inflation and the resilience of employment, and the Fed’s interest rate cut is expected to be delayed. Judging from the bitmap of the interest rate meeting in March and the expectations of the futures market, the Fed may cut interest rates at least three times in 2024 and start to cut interest rates as early as June. 2) In addition, in the early period, the Bank of Japan’s monetary policy turned, and the exchange rate of the yen was favorable, and the yen depreciated. As the second largest weight in the basket of currencies of the US dollar index, the yen led to the appreciation of the US dollar and the passive depreciation of the RMB.

Condition 2: The economy still has hidden worries, and it still needs wide monetary care.

1-2Most macro indicators in June were better than expected, but the performance of high-frequency indicators such as real estate and infrastructure was still weaker than the same period of last year, which needed the care of a wide currency.In January and February, most macro indicators such as CPI, industrial added value, investment in fixed assets, export and consumption were better than expected, but credit indicators such as social financing were lower than expected, and high-frequency indicators in real estate, infrastructure and other fields were still weaker than the same period of last year. Specifically, 1) although real estate investment converged to -9% in January and February, other related indicators of real estate (such as newly started area and sales area) are still in the double-digit decline range; 2) The growth rate of infrastructure investment in January and February was at a high level of 9%, but the rate of construction site resumption after the holiday was weaker than that in the same period of last year. The issue of special bonds and the net financing of urban investment bonds in the first quarter were not optimistic, and the growth rate of subsequent infrastructure may slow down.

Condition 3 of interest rate reduction: to solve the two major risks, it is also necessary to cooperate with a wide currency.

Looking back at history, risk resolution needs substantial support from liquidity.For example, during the period of 2015-2018, in order to cope with local hidden debts and high inventory of real estate, China issued a total of about 12 trillion replacement bonds, 2.65 trillion new special bonds, and 3 trillion net PSL, with a total scale of nearly 18 trillion, which is about 26% of GDP in 2015. At the same time, the one-year LPR quotation was reduced by 120BP.

Risk 1: In the process of localized debt, infrastructure investment may be under pressure, and the pressure of debt service will rise, which requires the cooperation of a wide currency.Under the current background of localized debt, the expansion of local debt, especially implicit debt financing, may be restricted. From the perspective of capital correlation, local implicit debt has the greatest impact on the growth rate of infrastructure. In 2024, infrastructure investment may be under pressure, and from the perspective of steady growth, it still needs the support of a wide currency. In addition, from the perspective of interest payment pressure, the balance of government debt is expected to increase by 13% in 2024, while the growth rate of generalized fiscal revenue and expenditure in 2024 is only 2.5% and 7.9%. In the case of no obvious decline in interest payment cost, the pressure of government interest payment may rise further. From the perspective of reducing the pressure of government debt repayment, it is necessary to cooperate with a wide currency.

Risk 2: the downward pressure on real estate is still great, and it needs wide currency support.Judging from the scale of real estate investment, the scale of China’s real estate investment in 2023 decreased by nearly 25% compared with the high point in 2021, while Japanese real estate investment peaked in 1996, with the highest cumulative decline of 54%. From the perspective of housing price, the price index of new houses and second-hand houses in 70 cities in China has fallen by about 5% and 10% respectively compared with the high point in 2021, while the average residential land price index in Japan has fallen by 47% compared with the high point. Judging from the level of residents’ leverage ratio, China’s residents’ leverage ratio is still consolidating, while Japan’s residents’ leverage ratio started rapid deleveraging in 1999, with the maximum leverage ratio of 12.6pct. To sum up, at present, the downside risk of China’s real estate is still large, which requires the support of a wide currency.

The following is the text

Since the first quarter, the interest rate of 10-year treasury bonds has been rapidly falling to around 2.3%, and it has continued to consolidate in the near future.It is difficult for the interest rate to exceed 2.3% in the short term. We believe that there are two main reasons: (1) Compared with the one-year MLF interest rate of 2.5%, the interest rate of 10-year government bonds has implied the expectation of interest rate reduction of 20BP. However, under the restriction of exchange rate, the Federal Reserve will not budge, so the probability of short-term interest rate reduction in China is low, and it may be difficult for interest rates to fall sharply again; (2) On the economic fundamentals, the macro data in January and February were disclosed one after another, among which the export, CPI, investment in fixed assets, industrial added value and other indicators were all better than expected, and the bond market rebounded due to the recovery of sentiment in the equity market and the seesaw effect of stock and debt. If the subsequent interest rate is to go down further, it may need the guidance of MLF to cut interest rates.

What are the conditions for the next rate cut? We answer this question from overseas, domestic and medium-and long-term perspectives.

Exchange rate and interest rate once again came to their respective low levels.Since the "811" exchange rate reform in 2015, the stages when the exchange rate and interest rate are at their respective relatively low levels are mainly from the end of 2016 to the beginning of 2017 and the beginning of 2020. The follow-up trend of the two stages is the upward trend of interest rate and the appreciation of exchange rate. The essential reason behind this is the improvement of economic fundamentals. However, at present, the domestic economy is still in a weak recovery stage, and the expectation of the Federal Reserve’s interest rate cut is delayed, so the supervision faces a dilemma between exchange rate and interest rate.

Is the American economy "soft landing" or "reflation"? When will the interest rate cut come?

The market had expected that the Federal Reserve would start to cut interest rates in the first quarter of 2024. In this regard, the US bond interest rate was expected to cut interest rates in advance and fell sharply in the fourth quarter of 2023; However, the recent expectations of the Federal Reserve to cut interest rates have been frustrated, and the interest rate of US bonds has also rebounded. The reason behind this is that the US economy is still resilient, which is manifested in the stubbornness of inflation and the resilience of employment.

From more perspectives: 1) American inventory cycle is at the bottom, and some industries such as retail and wholesale show signs of replenishment; 2) From the perspective of industry prosperity, both manufacturing and non-manufacturing PMI are at the bottom, and the consumer confidence index is obviously picking up. As the economy continues to exceed expectations and inflation is sticky, the market’s expectations for the US economy have shifted from a soft landing to re-inflation.

Cut interest rates at least three times in 2024, and cut interest rates as early as June. Judging from the bitmap of the interest rate meeting in March, the Federal Reserve expects to cut interest rates three times (25 BP each time) in 2024; Judging from the expectation of CME futures market, the market expects the Fed to cut interest rates as early as June. As the Federal Reserve starts to cut interest rates, the pressure of RMB exchange rate depreciation will be reduced, and the domestic wide monetary space will also be opened.

In addition, the shift of the Bank of Japan’s monetary policy in the previous period led to the depreciation of the yen and the appreciation of the US dollar, which is also one of the reasons for the recent depreciation of the RMB exchange rate. On March 19th, the Bank of Japan announced the adjustment of the monetary policy framework, decided to raise the short-term policy interest rate from -0.1% to 0-0.1%, and cancelled the yield curve control policy (YCC), and will guide the short-term interest rate as the main policy tool in the future. The yen’s exchange rate trading was full of benefits and depreciated rapidly after the monetary policy turned. As the second largest weight in the basket of currencies of the US dollar index, the depreciation of the Japanese yen makes the US dollar appreciate and the RMB passively depreciate.

1-2Most domestic macro indicators were better than expected in June.Judging from the data of the opening year, most macro indicators in January and February were better than expected, such as CPI of 0.7% (expected 0.4%), cumulative industrial added value of 7% (expected 4.3%), cumulative investment in fixed assets of 4.2% (expected 3%), cumulative social zero of 5.5% (expected 5.4%) and export (denominated in US dollars). However, credit indicators such as social financing were lower than expected. For example, in February, social financing increased by 1.5 trillion yuan (expected 2.4 trillion yuan) and the stock of social financing increased by 9% year-on-year (expected 9.1%).

However, some macro indicators deviate from micro high-frequency indicators, especially in the fields of real estate and infrastructure.From the perspective of high-frequency indicators, high-frequency indicators such as rebar output, cement delivery rate, cumulative transaction area of residential land in 100 cities and cumulative transaction area of commercial housing in 30 cities are still lower than the same period in 2023.

Specifically:

oneAlthough real estate investment converged to -9% in January and February, other related indicators of real estate are still in the double-digit decline range.In January and February, the newly started, constructed and completed housing areas were -31%, -11% and -21% respectively compared with the same period of last year. The national commercial housing sales area and sales volume were -25% and -32% respectively, and the real estate investment end and sales end were still in deep adjustment.

2From January to February, the growth rate of infrastructure investment (including electricity) was at a high level of 9%. However, judging from the situation of project resumption, the rate of post-holiday construction site resumption was weaker than that of the same period last year.According to the survey and statistics of Centennial Construction Network, as of March 12th, the rate of starting and returning to work and the rate of working on labor services in national construction sites were 75.4% and 72.4% respectively, which were 10.7pct and 11.5pct; lower than that in the same period of the lunar calendar in 2023. From January to February, the investment amount of the project also dropped by more than 40% compared with the same period of last year.

In addition, from the perspective of project funds, the current high growth rate of infrastructure may mainly come from the support of the trillion-dollar issuance of government bonds in 2023, but the situation of funds in the first quarter, especially special bonds and urban investment bonds, is not optimistic.

Credit funds increased slightly:In January-February 2024, the medium-and long-term loans of newly-added enterprises were 4.6 trillion yuan, 10 billion less than that of the same period of last year. If the proportion of medium-and long-term loans invested in infrastructure in January-February 2023 and January-February 2024 is estimated by using the proportion of medium-and long-term loans invested in infrastructure in Q1 2023 and 36% in the whole year of 2023 respectively, it is estimated that 167 billion yuan will be invested in infrastructure in January-February.

The issuance of new special bonds is slow:From January to March, 2024, a total of 634.2 billion new special bonds were issued, 722.6 billion less than the same period of last year, and the issuance progress was slow. Among them, the proportion invested in infrastructure (excluding infrastructure construction of municipal and industrial parks) is about 35%, which is slightly higher than the proportion invested in infrastructure in Q1 2023 (about 34%). The scale of special debt invested in infrastructure in January-March was about 237.9 billion less than that in the same period of last year, with a year-on-year growth rate of about -52%.

The net financing of urban investment bonds has been reduced:From January to March, the net financing of urban investment bonds was only 166.1 billion, a year-on-year decrease of 481.6 billion, with a year-on-year growth rate of -74%.

Generally speaking, the performance of domestic real estate is still weak, and infrastructure investment may also weaken under the background of localized debt. M1, the price level continues to run at a low level, and it still needs the active care of the wide currency to promote its low level recovery.

Looking back at history, risk resolution needs substantial support from liquidity.

During 1998-2004, faced with the impact of the Asian financial crisis and the high non-performing loan ratio in the banking industry, fiscal policy, on the one hand, issued a total of 210 billion treasury bonds for three consecutive years to expand government investment, on the other hand, issued 270 billion special treasury bonds to replenish bank capital. The total scale of the two debts accounted for 5.6% of GDP in 1998, and at the same time, monetary policy was greatly relaxed, and the one-year loan interest rate was reduced by 306BP.

During 2015-2018, the regulatory authorities actively solved the problem of hidden debts of local governments by "opening the front door and blocking the back door", and issued a total of about 12 trillion replacement debts, which made the local hidden debts explicit and gave local governments the right to issue bonds. During the period, they issued a total of 2.65 trillion new special debts. In addition, the regulatory authorities also realized the goal of real estate destocking through the monetization of shed reform, with a cumulative net investment of about 3 trillion PSL funds. The total scale of these funds is as high as nearly 18 trillion, which is about 26% of GDP in 2015. At the same time, monetary policy has remained loose during this period, and the one-year LPR quotation rate has been reduced by 120BP.

In 2023-2024, in the face of local debt risks and the downturn of the real estate cycle, it is estimated that 7.7 trillion yuan of new local special bonds will be issued, 1.5 trillion yuan of special refinancing bonds will be issued, 1 trillion yuan of additional government bonds will be issued, and 1 trillion yuan of special government bonds will be issued, and the accumulated PSL funds will be about 0.25 trillion yuan, totaling over 11 trillion yuan, which is about 9% of GDP in 2023. Since 2023, the one-year LPR quotation rate has been reduced by 20BP.

2024In 2006, we continued to face two major risks: local debt and real estate downturn. In the process of resolving the two major risks, we also need the cooperation of wide currency.

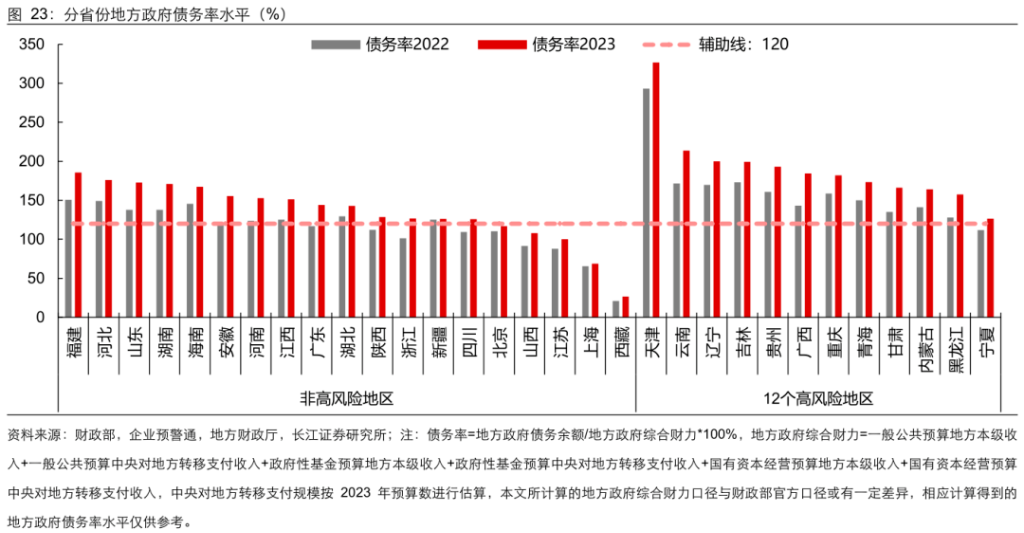

Risk 1: The local government debt pressure may still rise, which should not be underestimated.Compared with 2022, in 2023, the debt ratio of all provinces rose to varying degrees, among which the debt ratio of 12 high-risk areas was generally high and rose rapidly. In 2023, only the debt ratio of Beijing, Shanxi, Jiangsu, Shanghai and Xizang was within the warning line of 120%. In 2024, the scale of local special debt will still increase, but the pressure of local fiscal revenue is still there, and the debt pressure may continue to climb, and localized debt has a long way to go.

Risk 1: Under the background of debt conversion, infrastructure investment may be under pressure.Judging from the document "Measures for Strengthening the Management of Government Investment Projects by Classification in Key Provinces (Trial)" issued by the General Office of the State Council, the key debt-oriented provinces will strictly control the new government investment projects and strictly clean up and standardize the government investment projects under construction before the local debt risk drops to a medium or low level. Judging from the investment plan of major projects, the investment amount of key projects in 2024 in Inner Mongolia, Guangxi, Guizhou, Ningxia and other key debt-paying provinces and cities decreased significantly compared with that in 2023.

Risk 1: Infrastructure investment may be under pressure, and stable growth requires a wide currency.Under the current background of localized debt, the expansion of local debt, especially the financing of implicit debt, may be restricted, and from the perspective of capital correlation, local implicit debt has the greatest impact on the growth rate of infrastructure. At present, the proportion of hidden debts and infrastructure in 12 provinces is about 19% and 26%. In 2024, if the growth rates of hidden debt and infrastructure in 12 provinces are -5% and -5% respectively, and the growth rates of hidden debt and infrastructure in non-12 provinces are 8% and 10% respectively, the corresponding annual growth rates of hidden debt and infrastructure are 5.7% and 6.1% respectively.

Risk 1: the pressure of interest payment is rising, and wide finance also needs the cooperation of wide currency.In addition, from the pressure of interest payment, the interest payment expenditure of government bonds reached 1.9 trillion in 2023, accounting for 6.7% and 5.1% of the general fiscal revenue and expenditure, up by 0.4 and 0.3pct; year-on-year; In 2024, the balance of government debt is expected to increase by 13%, while the growth rate of generalized fiscal revenue and expenditure in 2024 is only 2.5% and 7.9%. Under the condition that the cost of interest payment has not decreased significantly, the pressure of government interest payment may further rise. Judging from the rhythm of bond issuance, the issuance of government bonds will start in May or will enter a peak period; Judging from the maturity of bonds, it is estimated that about 10 trillion government bonds will mature in 2024, which means that if the interest payment cost of new bonds after bond swap is reduced by 1BP, the interest payment will be saved by 10 billion. From the point of view of reducing the pressure of government debt repayment and reducing the cost of bond swap, wide finance needs the cooperation of wide currency.

Risk 2: Is the downside risk of real estate over? From the perspective of quantity.

From the perspective of housing demand,According to the calculation of Oriental Jincheng, the sales area corresponding to the demand for new housing in cities and towns in 2021-2025 is about 718 million square meters. Suppose that the center of China’s real estate sales area is about 1 billion square meters. Although the sales area of China’s real estate is close to the center level at this stage, the sales area of real estate above the center in the past decade or so has overdrawn some of the housing demand in subsequent years, and this part of the real estate bubble may take a long time to clear up.

Judging from the scale of real estate investment,In 2023, the scale of China’s real estate investment was about 11 trillion yuan, which was nearly 25% lower than the high point in 2021. Judging from Japan’s experience, Japan’s real estate investment peaked in 1996, and now it is stable at about 18 trillion yen, with a cumulative decline of nearly 40% from a higher point and a maximum cumulative decline of 54%.

Risk 2: Is the downside risk of real estate over? From the perspective of price.

From that perspective of house price,According to the data of Zhongyuan Real Estate, by the end of 2023, the prices of second-hand houses in Beijing, Shanghai, Guangzhou and Shenzhen had dropped by 17%, 19%, 18% and 31% respectively. The price index of new and second-hand houses in 70 cities disclosed by the Bureau of Statistics peaked in August 2021, and by February 2024, it had dropped by about 5% and 10% respectively. From the experience of Japan, the average residential land price index in Japan reached a high point in 1991, and then declined all the way. In 2023, the average residential land price index has fallen by 47% from a high point.

Residents’ income confidence is weak, and the expected decline in house prices accounts for a relatively high proportion.In addition, according to the results of the central bank’s questionnaire survey, in the fourth quarter of 2023, only 12.6% of residents thought that their income had "increased", down 1.2 percentage points from the previous quarter, and the residents’ confidence index for future income further fell to 47%; From the perspective of house price expectation, only 12% residents expect house prices to rise, while 20.2% residents expect house prices to continue to fall.

Risk 2: the downward pressure on real estate is still great, and it needs wide currency support.

Japan’s untimely policy response is one of the reasons why it has been lost for 20 years.The Economic White Paper issued by the Planning Department of Japan in 1992 holds that "the economic slowdown that began at the end of 1990 was mainly due to the influence of preventive monetary tightening and self-adjustment in the process of maintaining economic balance"; It was not until 1993 that the Japanese government realized that this economic downturn was different from the previous economic recession cycle. Japan’s discount rate changed from tight to loose in July 1991 and began to cut interest rates. In September 1993, the discount rate fell to 1.75%, which was lower than the lowest interest rate before the bubble burst, but it did not stop the downward trend of the real estate cycle. However, Japan’s land policy, which was tightened in the early stage, was not abolished until 1998. However, at this time, the impact of the bursting of the asset bubble on the behavior of residents and enterprises has been difficult to easily reverse, and the Japanese economy has fallen into a lost twenty years.

Judging from the leverage ratio of residents,The leverage ratio of Chinese residents has been consolidating at around 62% since it reached a high point in 2020; From the experience of Japan, after the bursting of the Japanese real estate bubble in 1990, the leverage ratio of Japanese residents was consolidating for a period of time. In 1999, it started rapid deleveraging and bottomed out in 2007, with a deleveraging rate of 12.6pct.

Generally speaking, the downside risk of China’s real estate industry may not be over yet, and it still needs the support of a wide currency.

In the second quarter, the above three factors may have marginal changes, thus pushing down interest rates.(1) From the market expectation, the Federal Reserve may start to cut interest rates in June, and the domestic RRR cut space may be gradually opened. (2) At present, domestic real estate investment and sales are still in a deep adjustment range. In the first quarter, the financial strength was less than expected, the issuance of special bonds was slow, the growth rate of infrastructure may be restricted, and the weak economic fundamentals may need further care from the broad currency. (3) From a medium-and long-term perspective, in the process of resolving local debt risks, for the needs of steady growth and reducing the cost of bond swap, or the cooperation of the central bank with a wide currency, and the real estate cycle has not yet reached an equilibrium level, the wide currency is still needed for support. Under the combination of "wide currency+weak fundamentals", interest rates may usher in new catalysis.

This article is from Wall Street. Welcome to download the APP to see more.